This article is the fourth part in a series from Roland Berger. It was written by Wolfgang Bernhart, Markus Baum, Falk Meissner, and Konstantin Shirokinskiy.

The automotive software market is changing with the rapid growth of software-enabled features in cars. The software spend of OEMs and suppliers is set to skyrocket by 2030 with shifting proportions of different software cost categories. A new, software-defined approach to car design has emerged: cars are built around software platforms rather than the incumbent approach of integrating software into cars. The shift in design philosophy will enable the auto industry to become more innovative and avoid almost USD 17 billion in costs annually. Transforming to the new approach isn’t straightforward. It requires new thinking, new technology and new business models.

Today’s automobile has become more than simply a way of getting from A to B. It has become a software-enabled feature-packed device – a computer on wheels. In Parts 1 and 2 of our Computer on Wheels series, we looked at how electronics and software are changing the automobile industry, turning OEMs into software players. In Part 3, we assessed the role of Tier 1 suppliers in the new landscape and how they need to adjust.

In this Part 4 we focus on the future software spend of automotive OEMs and their incumbent and new suppliers, and how they need to adapt. In particular, we look at how the industry’s transition from incumbent thinking (integrating software into cars) to a software-defined approach (building cars around software) will develop, and what opportunities it will create.

The value of cars and related services is increasingly dependent on software content, with the rollout of electric and ever-more autonomous vehicles driving this growth. More software means more complexity and challenges: new products, services and upgrades take a long time to develop and bring to market; they are hard to monetize after the initial sale; agile software development methods contradict traditional development cycles; testing, integration and maintenance costs are high; and it’s difficult to define future requirements.

These problems are largely rooted in the auto industry’s “Incumbent Approach” to building cars: fitting software into existing or new automotive models. This is increasingly complex, cumbersome, and therefore expensive, and hampers innovation. Most OEMs are now transitioning towards a “Software-Defined Vehicle (SDV) Approach”, where the software characterizes the hardware and the car is built around software platforms. In the following chapters, we look at the three key aspects of this approach: a scenario showing the future software spend and potential cost avoidance of shifting to a purely SDV approach; the required technologies, such as microservices; and potential future business models.

The value of cars and related services is increasingly dependent on software content. Automotive OEMs need to transition towards a Software-Defined Vehicle Approach, where the software shapes the hardware around it."

–Falk Meissner, Partner, Roland Berger

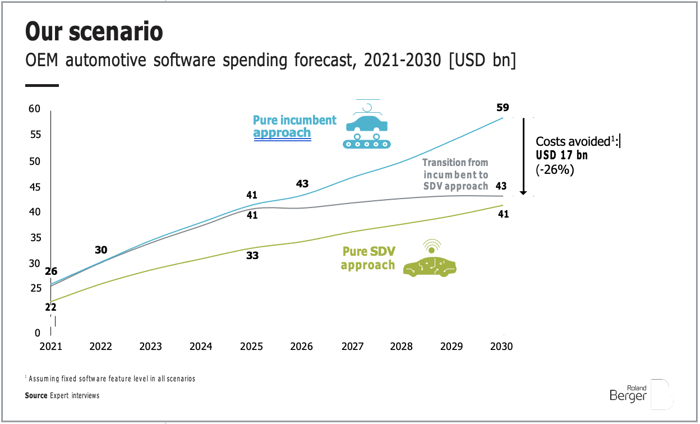

The transition to the SDV approach is a fundamental requirement for the automotive industry to meet complexity challenges and increase functional demand. It also represents a massive opportunity to boost value by generating efficiencies. Under the SDV approach, we expect the necessary software spend in the automotive industry1 ' to rise by 70% – from USD 26 billion in 2021 to USD 43 billion in 20302 (USD 327 to USD 575 per vehicle). Under the incumbent approach, the software spend is expected to more than double – from USD 26 billion to USD 59 billion in 2030 (USD 419 per vehicle). This means the SDV approach avoids costs of almost USD 17 billion per year and enables the industry to meet the coming challenges.

In both cases, the increase in software spend is driven by the increasing sophistication of infotainment (IVI) and advanced driver-assistance systems/autonomous driving (ADAS/AD), increased maintenance costs, and a rise in application development. This results in an increase of automotive software spend of 6% CAGR until 2030. Put bluntly, only by avoiding costs can the industry afford the software required in the future.

Below we assess the USD 17 billion cost avoidance achieved by the SDV approach versus the incumbent approach. For a 360-degree view, we approached this from three different angles – the software stack level, the domain level and in terms of development steps (development, integration, maintenance and testing). For each, we discuss how the projected costs alter the make-up of the total automobile software spend in 2030 compared to 2021.

.png?width=700&name=Costs%20by%20development%20step%20(Roland%20Berger).png)

.png?width=700&name=Costs%20by%20stack%20layer%20(Roland%20Berger).png)

.png?width=700&name=Costs%20by%20vehicle%20domain%20(Roland%20Berger).png) Stack level

Stack levelThe classic software stack is applicable to cars – hardware layer at the bottom, followed by operating system, middleware and services, topped by the application layer. In the SDV approach, the application layer is the source of almost all the avoided costs. The SDV approach lowers the high application development costs of the incumbent approach as integration and testing efforts are greatly reduced. The application layer contributes USD 14 billion of the almost USD 17 billion total cost avoidance offered by SDV approach. Reinvestment in application development will result in a CAGR of 7% in average for the overall application stack across all domains.

Infotainment and ADAS/AD are the two most complex vehicle domains, due to the complexity of the required signal processing, object detection and safety systems. They therefore benefit most from the SDV approach. Infotainment accounts for USD 7 billion in avoided costs versus the incumbent approach, and ADAS/AD slightly less at USD 5 billion, driven by the high costs of AI. This will drive the automotive software spend at a CAGR of about 8% for the AD/ADAS and IVI domains in particular.

Gauging costs by each step in the development cycle incorporates aspects of both the stack and domain levels. Initially, the SDV approach requires the setting up of more complex architectures (for example, microservice architectures – see box), resulting in increased development spending. This rise of around USD 7 billion is more than offset by big cost reductions in more agile software production: testing (USD 11 billion), integration (USD 8 billion) and maintenance costs (USD 3 billion). In addition, this frees up resources for content development.

In the SDV approach, the cost for maintaining and updating an increasing set of interdependent software over long periods after SOP, although lower than in the incumbent approach, remains a driver for growth, with a CAGR of 16%.

.png?width=700&name=Development%20costs%20(Roland%20Berger).png)

Microservice architectures (MSAs) enable the rapid, frequent and reliable delivery of large, complex applications. Agile teams of developers independently develop, maintain and improve new services (microservices), each linking into the whole through a pre-defined API (application programming interface) gateway. The benefits, compared to conventional monolithic architectures, include reduced interdependencies, increased system stability, faster times to market and a more organized development process.

Key assumptions

The model outlined above is based on two core assumptions:

Ultimately, OEMs that fail to change their approach will have a substantial competitive disadvantage: higher costs, lower customer value and most importantly, outdated products. In the next chapter we look at the technology required to successfully achieve the transition.

The incumbent approach aims to integrate software into a car, typically by adapting it to different models and configurations in a time-consuming process. This contradicts the lower effort, shorter time to market, efficient maintenance and reduced complexity requirements of software development. Therefore, the automotive industry needs to move away from today’s technology to a software-centric approach.

Benefits of the new approach

Today’s technology is characterized by a monolithic software architecture and a distributed E/E architecture, resulting in the following:

In contrast, the SDV approach is characterized by new service-oriented or microservice- based architectures (MSAs) and a central, zonal E/E architecture. Its key advantages stem from breaking down functions into independent, more manageable parts, enabling faster testing, validation and releases.

.png?width=700&name=Mono%20versus%20micro%20(Roland%20Berger).png)

"A Software-Defined Vehicle approach offers multiple advantages across all development steps and thus becomes a key success factor for automotive OEMs."

–Wolfgang Bernhart, Senior Partner, Roland Berger

Below we outline these advantages by development step, highlighting the drivers of avoided costs.

Development

Incumbent monolithic architectures rely on a single continuous string of code, which must be updated in its entirety even if only a small change needs to be made to a service. In new architectures, each service is independently developed and deployed, meaning changes only require updates to individual service-specific code within the parameters of the defined interface. In microservices, the use of individual microservice APIs and an API gateway allows services to communicate directly, independent of their chosen implementation. The definition of the APIs and designing services in such a highly independent structure requires high levels of effort, and therefore drives initial development costs.

Testing

The single binary file of monolithic architectures hampers testing, too. Whenever an upgrade or update is introduced, the entire application needs to be re-built and validated. This is not the case in MSAs: upgrades affect only individual microservices, reducing the need to test the overall application. The reduction in testing is the largest avoided cost of the SDV approach.

Integration

A key benefit of the SDV approach is the drastically reduced system integration efforts enabled by hardware abstraction and MSA. This is in contrast to monolithic applications, which must be completely re-built and taken offline to implement code changes.

Maintenance

The main advantage here is the ability to reuse code and incrementally adopt it (for example, in agile development and code maintenance) without having to integrate and test a whole new function or system. In addition, single points of failure have a far smaller impact in an MSA as they do not bring down the entire system right away.

So, in contrast to monolithic architectures, the overall effects of new architectures on software development are:

It is important to note that microservices are currently used only for non-safety critical functionality. However, we expect this to change in the medium term. As the ability to scale in-vehicle computing power increases and the availability of safety-certified container technologies widens, microservices are expected to be applied throughout all vehicle domains in the future.

The shift towards an SDV approach will have significant implications for the automobile industry. We find that the major automotive players already try to move away from monolithic architectures to multi-component or microservice architectures with a high degree of reuse. The major obstacle on their journey is, however, the management challenge to oversee and steer the vast amount of software developers working across millions of lines of code, says software development process expert Johannes Bohnet, CEO of Seerene. OEMs and suppliers need to transform to compete in the new market environment, meaning they must rethink their business models and role in the value chain – and they must be able to systematically drive the necessary transformation processes in their software development units.

How to remodel

Today, OEM software requirements are highly specific to their particular vehicle platform and architecture. Tier-1s and software suppliers provide customized solutions to individual OEMs, who usually own the IP. This creates inefficiencies as it drives-up integration and testing costs, prevents reselling of software, and therefore limits economies of scale.

The automotive industry needs to establish four key tenets of software-driven business model innovation: common standards, an open-source approach, IP trading and efficient IP management. Below we look at each.

The SDV approach enables OEMs and suppliers to update and extend their business models, as well as focus on economies of scale and state-of-the-art software. Our key recommendations are:

Microservice software architectures

Deploy new software architectures, such as microservice architectures, to reduce development complexity, integration, testing and maintenance efforts, as well as make use of continuous deployment.

Containerized middleware and applications

Implement containerized middleware to allow for continuous deployment and cloud- native design principles to run applications on the car and in the cloud.

Central + zonal E/E architecture

Develop central + zonal E/E architecture to provide a suitable hardware environment for the software-defined approach.

IP management & economies of scale

Set up a dedicated IP management unit incl. sufficient tools and processes to make use of economies of scale from trading IP/software with other players to maximize value generated by software functions.

Software-as-a-product

Suppliers should invest in in-house (platform) development, moving towards SaaP, and therefore bringing to market their own solutions while owning the software IP.

Software licensing

OEMs should monetize software architectures by selling/licensing them to other manufacturers, eventually partnering with OESs to leverage their distribution channels.

To enable an SDV approach, the automotive industry needs to establish common standards, an open- source approach, IP trading and efficient IP management.

–Konstantin Shirokinskiy, Partner, Roland Berger